How to Reduce Involuntary Churn in SaaS: 2026 Guide

Involuntary churn is defined as subscription cancellation caused by payment failures rather than a deliberate customer decision to leave. It accounts for 20–40% of total churn in B2B and B2C SaaS businesses, yet most founders treat it as a billing afterthought. That gap is expensive. To reduce involuntary churn in SaaS, you need a layered strategy that combines payment failure prevention, smart retry logic, and frictionless customer communication. This guide covers each layer in practical depth, so you can stop losing revenue to problems that are largely solvable.

What causes involuntary churn and how to measure it

Involuntary churn, also called passive churn or failed payment churn, has four primary causes: expired cards, insufficient funds, hard bank declines, and fraud flags. Each cause requires a different response, which is why grouping them under a single “payment failure” label is a strategic mistake. Expired cards are the most recoverable. Hard declines, where the bank permanently rejects the transaction, are not.

Measuring involuntary churn accurately starts with separating it from voluntary cancellations in your analytics. Failing to separate these churn types leads to misallocated retention efforts. A customer success team chasing product feedback from someone who simply had an expired card is wasting time that could go toward actual at-risk accounts. Stripe makes this separation possible through webhook events. The invoice.payment_failed event tags each failed charge with a decline code, giving you the raw data to classify churn by cause.

The most useful metric to track is your involuntary churn recovery rate by decline code. Best-in-class SaaS companies reduce involuntary churn to under 0.5% monthly through automated recovery. That benchmark is achievable, but only if your measurement is clean enough to tell you where recovery is failing.

Pro Tip: Build a simple dashboard that segments failed payments by decline code weekly. Expired card failures trending upward in a given month usually signal a card cohort approaching expiry, giving you a two-week window to act before revenue is lost.

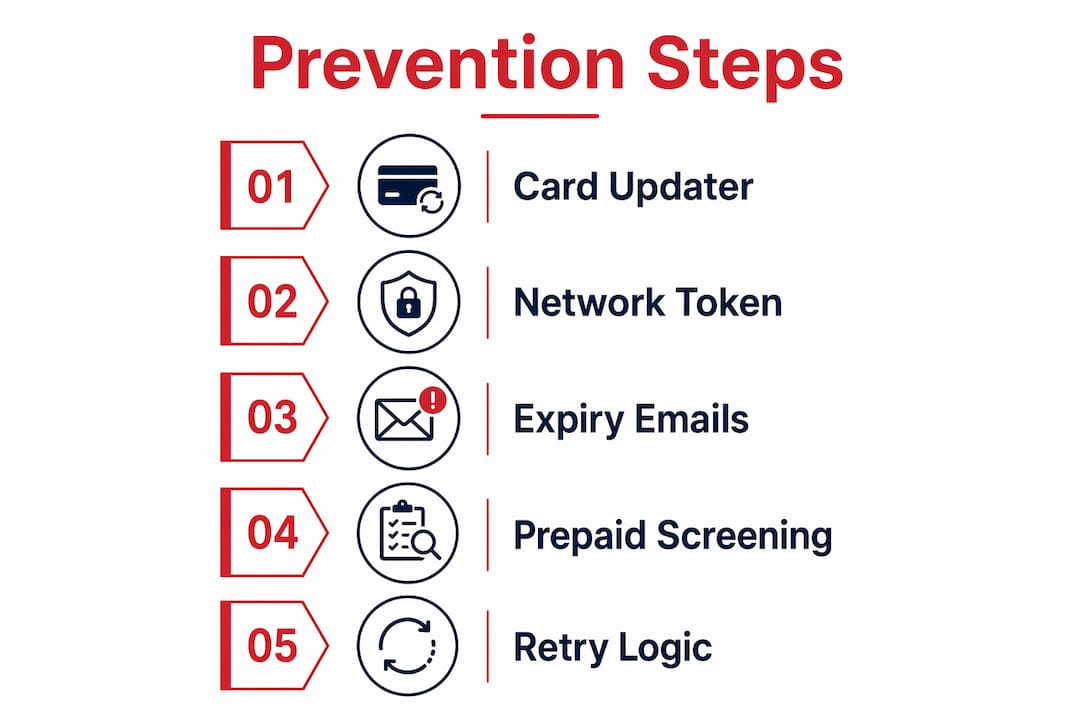

Which prevention tools significantly reduce involuntary churn rates

Prevention is more cost-effective than recovery. The three tools that deliver the most measurable impact are Card Account Updater (CAU) services, network tokenization, and proactive expiry notifications.

Card Account Updater services, available through Stripe and Braintree, automatically refresh card details when a card is replaced or reissued. This happens silently, before a payment attempt fails. CAU services prevent 5–15% of involuntary churn without any customer-facing friction. That range may sound modest, but at scale it represents thousands of dollars in ARR that would otherwise require active recovery efforts.

Network tokenization goes one step further. Instead of storing a static card number, the payment processor stores a network token that updates automatically when the underlying card changes. This is particularly valuable for customers who replace cards frequently, such as those using corporate cards with annual reissues.

Proactive card expiry emails are the third pillar of prevention. Sending a plain, direct email 30 days before a card expires prevents 30–50% of expiry-related payment failures. That is a significant reduction achievable with a single automated workflow. The email should include a one-click link to update payment details, with no login required. Friction at this step is the difference between a customer who updates their card in 90 seconds and one who closes the tab and never returns.

One prevention step that most SaaS companies skip is prepaid card screening at signup. Prepaid cards predict higher involuntary churn because they carry fixed balances and cannot be auto-updated by CAU services. Identifying and rerouting prepaid card signups to alternative payment methods, such as ACH or PayPal, removes a structural churn risk before it ever appears in your metrics.

| Prevention Method | Churn Impact | Implementation Complexity |

|---|---|---|

| Card Account Updater | Prevents 5–15% of involuntary churn | Low (enable in Stripe dashboard) |

| Network Tokenization | Reduces card replacement failures | Medium (requires processor support) |

| Expiry Email (30 days out) | Prevents 30–50% of expiry failures | Low (single automated workflow) |

| Prepaid Card Screening | Eliminates a structural risk segment | Medium (requires BIN lookup at signup) |

Pro Tip: Use a BIN (Bank Identification Number) lookup API at the point of payment entry to detect prepaid cards in real time. Offer ACH or PayPal as alternatives before the customer completes signup, rather than discovering the problem at the first billing cycle.

How to optimize smart retry logic for payment failures

Retry logic is where most SaaS companies leave significant recovery revenue on the table. The default Stripe retry schedule is a starting point, not an optimized strategy. Custom retry schedules based on decline codes consistently outperform default settings because they match retry timing to the actual reason for failure.

The logic works as follows. Network errors and temporary processor issues warrant a same-day retry, often within a few hours. These failures are infrastructure-level and resolve quickly. Soft declines, such as “do not honor” responses from a bank, typically require a 3-day delay before retrying. The bank is signaling a temporary restriction, and retrying immediately damages your processor reputation without improving recovery odds.

Insufficient funds failures require the most nuanced timing. Recovery rates of 55–70% are achievable when retries align with customer pay cycles. Scheduling retries for the 1st and 15th of the month, or on Fridays, captures customers immediately after payroll deposits. This single adjustment can meaningfully lift recovery rates for this failure category.

Hard declines are a different matter entirely. Retrying a hard decline wastes a charge attempt and signals to your payment processor that you are ignoring decline codes. The correct response to a hard decline is to immediately route the customer into a communication flow that requests a new payment method, not to retry the failed one.

Extending the Stripe retry window to 28 days recovers an additional 10–15% of failed payments. Many customers update their cards within two to three weeks of a failure, especially after receiving your dunning emails. A retry window that closes at 7 or 14 days misses those recoveries entirely.

What communication practices improve payment recovery rates

The majority of involuntary churn is not caused by the payment failure itself. It is caused by poor, delayed, or friction-heavy communication afterward. A customer who fails a payment and receives a confusing, branded HTML email with no clear next step will churn. The same customer who receives a short, direct message with a one-click update link will often recover within minutes.

Plain-text dunning emails sent from a founder’s personal email convert 2–3x better than branded HTML emails. This is counterintuitive for teams that have invested in brand design, but the data is consistent. Personal, low-friction messages feel human. They do not trigger spam filters. They communicate urgency without feeling like a marketing campaign.

Timing is equally critical. Emails sent within one hour of payment failure achieve 2–3x higher open rates than delayed notifications. The customer is still in a context where they are thinking about your product. Waiting 24 hours to send the first message allows that window to close. The recommended follow-up cadence is day 1 (within the hour), day 3, day 7, and day 12.

In-app banners and notifications reinforce email outreach without replacing it. A persistent, non-intrusive banner that appears when a user logs in after a failed payment, with a direct link to update billing details, captures customers who missed the email. The message should be short: acknowledge the issue, state the consequence of inaction, and provide a single clear step.

Pro Tip: Generate a tokenized, one-click payment update URL for each failed customer. This URL should bypass the login screen entirely and land the customer directly on the billing update page. Removing the login step alone can lift update completion rates significantly.

For customers who were not recovered during the dunning window, a separate reactivation email performs better than a standard win-back campaign. Reactivation rates are 2–3x higher when the message explicitly acknowledges the payment issue and provides a one-click reactivation link, rather than leading with promotional messaging.

How to analyze and strengthen your churn reduction strategy

Segmentation is the foundation of a mature involuntary churn reduction program. Treating all failed payments as a single cohort produces average results. Segmenting customers by payment method and failure cause allows you to deploy focused outreach and retry strategies that match the actual problem.

Start by separating your failed payment pool into three groups: expired cards, soft declines, and hard declines. Each group has a different recovery probability and a different optimal response. Expired card customers are your highest-value recovery targets. Hard decline customers need immediate human review to determine whether the account is worth pursuing with a new payment method request.

Automated dunning tools like Baremetrics Recover handle pre-dunning, multiple retry attempts, and follow-up communications in a single workflow. Baremetrics Recover recovers 40–60% of failed payments on average. One documented case reduced involuntary churn from 12% to 2% in three months, recovering over $50,000 in ARR. These tools are worth evaluating once your monthly recurring revenue makes manual management impractical.

The most common mistake in this phase is treating payment failures as product fit problems. When a customer churns involuntarily and the customer success team responds with a product feedback survey, it signals a measurement failure upstream. Clean churn classification prevents this misallocation.

| Approach | Recovery Focus | Risk |

|---|---|---|

| Aggressive retries (all failure types) | Maximizes attempt volume | Damages processor reputation; harms approval rates |

| Decline-code-specific retries | Targets recoverable failures only | Requires webhook integration and custom logic |

| Communication-only recovery | Low technical overhead | Lower recovery rates without retry support |

| Combined retry and dunning automation | Highest overall recovery rate | Higher setup cost; requires ongoing monitoring |

The part of involuntary churn that most guides ignore

Most articles on minimizing involuntary churn focus on the mechanics: retry schedules, webhook events, CAU activation. Those mechanics matter. But in my experience working with SaaS founders, the biggest gap is almost never technical. It is the assumption that a working system does not need to be watched.

Automated dunning tools and retry logic are not set-and-forget infrastructure. Decline code patterns shift. Card networks update their rules. A retry schedule that performed well six months ago may be generating unnecessary processor friction today. The teams that consistently achieve the lowest passive churn rates are the ones that review their recovery dashboards monthly and test communication variants quarterly.

The second thing most guides understate is the cost of a bad customer experience during recovery. A customer who feels pressured, confused, or embarrassed by a payment failure communication is more likely to cancel voluntarily after the payment is recovered. The goal is not just to collect the payment. The goal is to collect the payment in a way that leaves the customer feeling respected. Short, clear, human-sounding messages accomplish this. Aggressive multi-touch sequences that escalate in urgency every 48 hours do not.

Prepaid card screening at signup is the one prevention step I consistently see overlooked, even by teams that have invested in CAU and tokenization. Identifying prepaid cards before the first billing cycle costs almost nothing to implement and eliminates a predictable churn segment before it ever appears in your recovery queue.

— Raymond

How E-regency helps SaaS founders retain more revenue

Reducing passive churn requires more than a checklist. It requires a clear view of where your payment failures are concentrated, why they are happening, and which recovery levers will move the needle for your specific customer base.

E-regency Advisory combines AI-driven customer health modeling with hands-on retention strategy optimization to help SaaS founders move from reactive billing management to proactive revenue protection. Clients have reported gross churn reductions of over 20% and net revenue retention increases above 115%. If you are ready to build a recovery framework that fits your current stage, schedule a strategy session with the E-regency team to identify your highest-impact opportunities.

FAQ

What is involuntary churn in SaaS?

Involuntary churn is subscription cancellation caused by payment failures, such as expired cards or insufficient funds, rather than a customer’s deliberate decision to cancel. It accounts for 20–40% of total churn in most SaaS businesses.

How do i separate involuntary churn from voluntary churn?

Use Stripe webhook events, specifically invoice.payment_failed, to tag each failed charge with a decline code and classify it separately from voluntary cancellations. Clean classification is the prerequisite for targeted recovery.

What is the best retry timing for insufficient funds failures?

Schedule retries on the 1st and 15th of the month, or on Fridays, to align with common payroll deposit dates. This payday-aligned approach achieves 55–70% recovery rates for this failure type.

How long should my stripe retry window be?

Extend your retry window to the maximum 28 days. Extending to 28 days recovers an additional 10–15% of failed payments that would be missed by shorter default windows.

Do plain-text emails really outperform branded HTML emails for dunning?

Yes. Plain-text emails sent from a founder’s address with a direct payment update link convert 2–3x better than branded HTML emails because they feel personal, avoid spam filters, and reduce friction to a single clear action.

Key takeaways

Reducing involuntary churn in SaaS requires combining payment failure prevention, decline-code-specific retry logic, and frictionless customer communication into a single, continuously monitored recovery system.

| Point | Details |

|---|---|

| Measure churn types separately | Tag failed payments via Stripe webhooks to separate involuntary from voluntary churn before acting. |

| Activate prevention tools first | Enable Card Account Updater and send expiry emails 30 days out to stop failures before they occur. |

| Match retry timing to decline codes | Use payday-aligned retries for insufficient funds and avoid retrying hard declines entirely. |

| Send plain-text emails within one hour | Personal, low-friction messages sent immediately after failure recover payments at 2–3x the rate of branded emails. |

| Screen prepaid cards at signup | Detect prepaid cards using a BIN lookup API and redirect those customers to ACH or PayPal to eliminate a structural churn risk. |